The complete guide to small business tax season (2026)

So many small business owners dread tax season. Not only does it mean extra work on your plate, the fear of getting audited if you make a mistake is really stressful.

But there’s a different way to think about tax season. All the extra work you’re doing at this time of year can actually teach you a lot about your business, and help you plan better for the year to come.

We built this guide to help you with three key things that will reduce your stress and give you insight into your business:

- To help you prepare your books properly for your accountant so that they can help you save as much money as possible.

- To demystify audits so you can prevent them, handle them when they happen, and stop fearing them.

- To teach you how to stay on top of your books year-round, so you won’t procrastinate and panic at tax time anymore.

Chapter 1: Understanding common tax deductions that save you money

Tax season can be stressful—especially for small businesses. But it’s also a huge opportunity for entrepreneurs to dig deep into their business’s finances and performance and set themselves up for success in the coming year.

Business tax deductions are a big part of that because they can save valuable funds you can use to grow your business. According to the latest data available from the Internal Revenue Service (IRS), business tax deductions for 2022 totalled over $1.4 trillion. That’s one big opportunity!

Understanding the tax deductions your business is eligible for goes a long way in ensuring you save every dollar possible. Even if you hand off tax preparation to a professional, it’s important to know your deductions so you can prepare and keep the appropriate records to claim them.

In this chapter, we’ll run through:

- How tax deductions work

- Deductions all self-employed workers and small business owners should know

- Common mistakes to avoid when you deduct business expenses

How do tax deductions work?

In a nutshell, tax deductions (also called write-offs) are one way taxpayers can lower their tax liability or the amount of tax they pay. When you prepare and file your taxes, you claim the deductions your business qualifies for on your annual tax return.

Deductions come in all varieties, but they have one thing in common—they count against and reduce your total taxable income. That’s different from a tax credit, which counts dollar-for-dollar against your tax liability for the year.

For example, if your business income for last year was $100,000 and you claim $20,000 in write-offs, your taxable income is $80,000. Your savings from those deductions are the total deduction amount ($20,000) multiplied by the tax rate for your income bracket. If your rate is 25%, for example, those deductions would save you $5,000 on your taxes for that year.

Deductions for self-employed workers

Independent contractors, freelancers, and sole proprietors are all considered self-employed workers in the eyes of the IRS.

What does that mean? At the most basic level, being self-employed means you don’t report to someone above you. From a tax perspective, self-employed workers typically pay quarterly estimated taxes that cover income tax and the additional self-employment tax.

For an individual, those taxes can add up in a hurry. That’s why it’s important to understand the six deductions we’ll cover next—so you can be ready to claim them and lessen the burden once tax season rolls around.

1. Home office deduction

The home office tax deduction is probably one of the most well-known and least understood deductions available to self-employed people. In a nutshell, this deduction is aimed at giving you credit for expenses associated with maintaining an office in your home.

It can be a substantial annual deduction, so it’s a wonder why more self-employed workers don’t claim it.

The costs of maintaining a workspace in your home can really add up, so if you’re eligible, the home office deduction is well-worth the time spent calculating it. You can deduct a percentage of home office expenses relating to:

- Rent or mortgage

- Renters’ or homeowners’ insurance

- Property taxes

- Internet and utilities

- Leasehold Improvements

Not to mention, the IRS instituted a standard rate for home office deductions, creating a much faster and simpler method for calculating your deduction amount. The rate is $5 per square foot of office space, up to a maximum deduction for 300 square feet or $1,500.

Your home office space only needs to meet two main requirements to qualify for the deduction:

- The space has to be used to conduct business regularly and exclusively, meaning you can’t claim an entire room if it actually doubles as the guest room.

- Your home office needs to be your primary place of business. If you head to the coffee shop from time to time, that’s okay.

If you rent an office space outside your home, see the Rent and utilities section under small business deductions.

2. Legal and professional fees

There are some aspects of running a business that are better handled by experts. When you work with a professional to handle something (like an accountant to file your taxes or a lawyer to incorporate your business), you can deduct the cost of their help.

The deduction includes professionals of every stripe, including:

- Lawyers

- Accountants

- Bookkeepers

- Consultants

- Independent contractors

- Appraisers

- Systems analysts

It’s important to note: you can only deduct professional fees that are directly related to your business. For example, if you hire an accountant to file both your personal and business taxes, you can deduct only the cost of your business tax filing.

3. Your own benefits

For some self-employed workers, health insurance, retirement savings, and other benefits you’d otherwise receive from an employer can easily become your biggest expenses. That’s why they are also typically eligible as deductions from your taxes. The most significant (and frequently evolving) deduction is for health insurance premiums.

You can deduct all premiums for health, dental, and long-term care insurance for you, your spouse, and any dependent children under 27 years old. Most self-employed workers are eligible, but you may not qualify if:

- You or your spouse were eligible for an employer-provided health insurance plan

- You did not purchase qualifying insurance

The amount of the deduction may not exceed the earned income from your trade or business minus the deductions for one-half of self-employment tax and qualified retirement plan contributions.

In addition to health insurance and retirement contributions, you can also deduct other common types of insurance you may need as a solopreneur—including professional liability insurance, disability insurance, and home-based business insurance.

4. Business-related education

If you pursue additional education to either maintain or improve skills that relate directly to your business or your legal ability to continue in the field, you may be able to deduct the cost of that education.

For example, an SEO consultant can deduct the cost of a course on what’s new for SEO. The IRS Publication 970 offers more guidance on expenses that do and do not qualify. However, this deduction is one that gets pretty specific, so we recommend working with a tax professional to see if you’re eligible.

For self-employed workers, the education deduction actually lowers your taxable income (instead of being credited against your tax liability), so it’s well-worth taking if your expenses qualify.

Note: Many taxpayers are also eligible to deduct any interest paid against your student loans. You should receive a 1098-E form from the lender, which includes the total interest you can deduct. The maximum deduction allowed for tax year 2025 is $2,500.

5. Travel

A family vacation to Maui unfortunately does not qualify for a business tax deduction. But any travel you do to meet with or acquire clients, perform services or deliver products, and attend conferences, seminars, and other education or networking events is a deductible travel expense.

Business travel has to be reasonably and demonstrably related to your business, of course, and you can write off all expenses including:

- Transportation (airfare, train fare, bus fare, Uber/Lyft/taxi fare, rental car, and auto mileage)

- Travel by airplane, train, bus or car between your home and your business destination

- Fares for taxis or other types of transportation between the airport or train station and your hotel, the hotel and the work location, and from one customer to another, or from one place of business to another

- Using your car while at your business destination. You can deduct actual expenses or the standard mileage rate, as well as business-related tolls and parking fees. If you rent a car, you can deduct only the business-use portion for the expenses

- Meals and lodging

- Accommodations (hotel or Airbnb)

- Meals for clients or customers

The key to appropriately deducting business travel expenses is to be reasonable. The IRS is vigilant about ensuring your deductions are legitimate business necessities. That means trying to deduct a 10-day family vacation where you met with one client won’t fly.

Keep accurate and plentiful records, and use a degree of reasonableness to substantiate your deductions.

6. Merchant processing and service fees

Self-employment means you’re accepting payments from clients or customers. Depending on the payment methods you accept—and the tools you use to process them—you’re responsible for merchant processing and service fees on those payments.

For example, typical credit card processors charge between 2.5% – 4% of the transaction amount. Those fees can definitely add up throughout the year, so it’s important to keep a record of every transaction. Those records enable you to deduct merchant processing fees from your business income.

Deductions for small businesses

Small businesses represent the vast majority of firms in the United States. They drive job creation and economic growth—they also contribute a lot to annual tax revenue.

Because small business and entrepreneurship is such a vital part of our economy, there are several tax deductions that can help lessen the burden on small businesses. In fact, many different business expenses can be deducted from your business taxes, including rent and utilities for your office and even invoices and bills that go unpaid.

1. Rent and utilities

Whether you rent a physical office space for 50 or one desk in the co-working space downtown, both your rent and any utilities for the office are deductible business expenses. Utilities include: electricity, gas, water, telephone, and internet bills.

If you work out of your home you can still deduct some of these expenses as they relate to your business use of the space. See the Home office deduction section above for more.

2. Equipment

Running a business involves a lot of equipment—even if it’s just you and your partner. Luckily, you can deduct almost any equipment your business requires, including:

- Computers and laptops

- Printers, copiers, and fax machines

- Desks, filing cabinets, and other office supplies like paper, pens, and Post-It notes

- Software

- Vehicles

- Any specialized equipment unique to your industry (like a heat press machine for a company that sells novelty t-shirts)

For the bigger ticket equipment, you can choose to deduct the full value in the same year you buy it or spread the cost out over a number of years (depending on the type of item).

3. Employee salaries, wages, and benefits

Self-employed workers can deduct their own benefit and insurance premiums, and the same applies to small business owners.

If you have employees, you can also deduct their salaries (including wages and bonuses) and any benefits you provide to them and their families.

4. Advertising expenses

Marketing and advertising for a small business can include a whole, wide swatch of tactics—all of which can be deducted as advertising expenses for your business. If you’re drawing a blank, here are some of the most common advertising expenses for today’s small businesses:

- Business cards

- Branded swag (from pens to popsockets)

- Website costs (including domain registration, site hosting, and design)

- Digital advertising (like social media ads, paid content, and PPC ads)

Everything from business cards to Facebook ads to billboards counts toward this deduction, so be sure to keep records on all your advertising expenses throughout the year.

5. Business insurance

As your small business grows, there are several different types of insurance you’ll need—from professional liability insurance to workers’ compensation and product liability insurance. The premiums for any insurance policies your business needs are deductible, similar to your health insurance deductible.

6. Bad debts

In any business, you have to account for some customers or clients who simply won’t make good on promises to pay. While you can’t magically make everyone pay their bills, the good news is you can deduct bad debts from your annual business taxes. Here’s what the IRS considers eligible for the bad debts deduction:

- Money you’ve loaned to other businesses, employees, or vendors

- Unpaid purchases of goods and services

Common mistakes to avoid when you deduct business expenses

Understanding the tax deductions that are available to you and your business is the first step in winning the year-end season. When you make the most of the deductions you qualify for, you’re lowering your tax burden and saving money—money you can put right back into your business (or money you can use to fund a little break from your business).

But there are a few common mistakes both self-employed workers and small businesses fall into, and they can end up costing you. Here are some of the mistakes we see with tax deductions—keep them in mind so you can avoid falling into these traps.

Failing to document and record

No matter which business tax deductions you claim on your taxes, they all have one thing in common: you need proof.

Deductions can be lucrative, so there are always people who erroneously claim tax credits and deductions they don’t qualify for. If your business is audited by the IRS, you’ll need documentation to back up every deduction you claim. That’s why it’s absolutely vital that you always document and record all of your business’ expenses, especially those you claim on your tax return.

You file taxes once a year—which means you have to remember and keep track of documentation for a good while before it comes in handy. You have a lot on your plate, and we know it’s easy for invoices to disappear and receipts to fall through the cracks.

That’s why we always recommend having a system in place to organize and manage your expenses and receipts. If you’re already using Wave, you can upload and categorize receipts*.

You can also sync your business bank account** with the Pro Plan to automatically import expenses.

Not claiming all the deductions you’re eligible for

That average small business or solopreneur qualifies for several tax deductions, and it’s in your best interest to claim every deduction you qualify for.

There are a few things that might keep you from claiming a deduction that you qualify for:

- Uncertainty whether or not you’re eligible for the deduction

- Complexity around claiming and backing up the claim

- Complicated calculations to determine the amount of the deduction for your business

Some deductions (like the home office deduction or equipment depreciation) require more complex calculations to figure out the actual amount of your deduction. But the bottom line is, if you forego deductions you qualify for, you’re losing out.

It can be complicated, and we get that—which brings us to the next all-too-common mistake…

Not working with an accountant or tax professional

A lot goes into preparing and filing your annual business taxes. It’s a complex topic—one that changes frequently, too.

While some small business owners can and do handle personal taxes by themselves (or with the help of DIY software, at least), business taxes are a horse of an entirely different color. It’s important for business owners to understand all that business taxes entail, but there’s a lot at stake when it comes time to actually file.

From mistakes that trigger an audit to leaving money on the table, your business is better off when a tax professional handles things. And now that you know the fees you pay for a professional accountant are tax deductible, there’s no reason to make this mistake.

We suggest filing your taxes with H&R Block if you’re based in the US. You can import your Wave accounting data straight into H&R Block and get set up with a personal tax pro specialized in small businesses to either do your tax filing for you or just help you out whenever you need it.

You’ll cut down hours of work, receive personal 1:1 advice, get all the latest info on tax deductions, and much more.

Fearing the audit

In the world of taxes, audit is a four-letter word. Taxpayers live in fear of the IRS audit—including the inconvenience and potential penalties it implies. But you don’t need to fear the audit, and you definitely shouldn’t let fear of the audit stop you from claiming deductions you’ve rightly earned.

There are two main defenses against an IRS audit: comprehensive records and professional tax filing. If you claim only the deductions you qualify for and you have documentation to back you up, you’re in good shape even if the IRS does choose to audit your return.

Since we’ve already talked about both of those defenses, your audits fears can float right out the window.

Understand your tax deductions

Most small business owners and solopreneurs don’t get excited about taxes—but deductions are one thing you should get excited about. After all, they’re all about scoring you valuable tax savings you can use to grow your business. If you have a solid understanding of the business deductions you may qualify for and seek professional tax help, you’ll be off and spending those savings in no time.

Want to test your knowledge for this guide? Try out our tax quiz on deductions: Can I Claim This?

Chapter 2: Preparing for a smooth year end

For small business owners and independent workers, the end of the year means closing your books and taking stock of your business. Wrapping up your annual accounting is about more than just preparing for taxes—it can be a powerful opportunity to take an in-depth look at your business and finances and find opportunities to continuously improve year over year.

Did your revenue grow over the last year? What can you do to continue that growth into the new year? How can you improve cash flow?

Asking these questions is a vital exercise for business owners, but it can easily get lost at the end of year. Between reconciling your books, getting a handle on tax documents, and planning for the year ahead, there’s a lot to do. Throw in holiday planning and your schedule can get downright oppressive.

That’s why it’s best to prepare for year end accounting ahead of time and plan for a smooth end to the year.

To that end, in this chapter, we’ll cover:

- Steps to take before you visit your accountant for year end,

- Year end period adjustments to make,

- Documents and information to gather and bring with you, and

- Key questions to ask your accountant.

Let’s get started!

What to do before you visit your accountant for year end

Accountants can sometimes seem like magicians—able to make sense of spreadsheets and numbers that read like hieroglyphics to the rest of us. But there’s one thing that can stand in the way of even the most magical and talented accountant: unfinished and disorganized bookkeeping.

If your business and financial records are a mess, it’s a lot harder (and maybe impossible) for an accountant to make sense of them. That’s why your first step, before you knock on your accountant’s door, is to get all of your books and records in order and up to date.

Before you set about reconciling your books, it’s important to ensure they’re closed on the year—meaning all of the transactions and entries are completed and recorded in your general ledger. That includes:

- Paying off all outstanding expenses and recording those expenses you’ve used but haven’t paid for yet

- Sending out final invoices and following up on unpaid and overdue invoices

- Recording all of your income for the year

- Running your last payroll (if you have employees)

- Categorizing and verifying all income and expenses within your accounting software of choice (if you use one)

Reconcile your transactions

Once all of your transactions have been entered and verified, the next step is to reconcile your accounts.

Simply put, run through to ensure all entries in your bank and credit card statements are included and correct in your accounting ledger—and vice versa.

Reconciling is an important part of making sure you aren’t missing information or working with inaccurate numbers.

Making year end period adjustments

Now that you know everything matches up, you’ll make your year end period adjustments. These adjustments help you account for things like bad debts and depreciation on your assets.

Period adjustments are a way for you to tie up the relationship between your costs and the revenue they generate. That makes for a better, more accurate and holistic picture of your business finances and performance—one you can act and make decisions based on.

Here are a few of the period adjustments you may need to make.

Bad debt adjustments

Our 2021 survey found that 1 in 4 micro business owners report waiting over a year to be paid - or not receiving payments at all.

Sad as it is, unpaid invoices are a reality of the freelance and small business worlds.

When you create an invoice, your books show that amount as income.

If the income never actually materializes (i.e. the customers just don’t pay), you need to adjust your books to write off those invoices. For Wave users, here’s a guide on how to write off an invoice.

Depreciation

When you buy certain equipment or other necessities for your business, they add to your business assets. But equipment like computers or vehicles depreciates over time and use—meaning the value of your assets goes down. You need to record that change in value to get a more accurate picture of your business’ assets.

Depreciation adjustments can be a little complicated, so we recommend working together with your accountant to decide on the best depreciation approach for your business, and how to record it on your books.

Accrued revenue and expenses

Accrued revenue and expenses are income and liabilities you’ve earned or used, but haven’t yet paid or been paid for.

For example, if you complete a client project on December 30th and don’t have a chance to invoice for it until January 3rd, you still want that revenue to be credited for the year in which you earned it. The same is true for expenses that you use in one year and pay for the next—like your business credit card bill for December, which you’ll pay in January.

Prepaid expenses

On the flip side of accrued revenue and expenses, there are some expenses you pay for before you use them.

Consider expenses like internet service. Your bill comes in December and covers your service for the upcoming month of January. If you make the payment before the year ends, you’ve prepaid for an expense in the following year. Recording this prepayment helps keep your expenses and the revenue they generate matched up.

Customer deposits

Whenever a customer or client pays all or part of your invoice before you actually complete the work, they’ve made a deposit.

That money isn’t technically income until you complete the work or ship the product, even though it’s sitting in your bank account. At year’s end, you’ll record any customer deposits as business liabilities because you’re obligated to do the work.

Documents, records, and reports to bring with you

Now that your books are all in order, let’s talk about the documents, records, and reports you need to bring along when you meet with your accountant. Various documents and reports can help your accountant get the best picture of your business and its financial health—not to mention helping them prepare for tax time.

When you meet at the end of the year, it’s always best to bring your tax return from the previous year. Your return has key information about your income, expenses, and the deductions you took that can help you compare how your financial situation and business performance has changed over the last year.

The more information you can bring to your accountant, the more productive your meeting will be. The documents and records you should bring fall into three main categories:

- Basic financial reports,

- Business expense records, and

- Tax forms

Let’s talk about what each of those involves.

Basic financial reports

Your accounting information and basic financial reports work together to give your accountant a more holistic picture of your business finances over the past year. They can tell them things like how healthy your cash flow was, how much revenue you brought in, and whether you had a profit or loss this year.

These are the three financial reports you definitely need to bring:

- Balance sheet

- Income statement (or profit and loss report)

- Statement of cash flow

In addition to those official financial reports, we also recommend bringing along a copy of your trial balance at year end and your general ledger. Remember, the more information your accountant has, the better advice they can give.

Business expense records

Your financial reports give your accountant a good overview, but it’s also helpful to drill down into some of the details around where and why your business is spending the money you’re spending. That’s why comprehensive records of all your expenses for the year can be so helpful.

That includes documentation like receipts, bills, bank and credit card statements for expenses like:

- The quarterly estimated taxes you paid

- Your payroll records for the year

- Other business expenses (like the rent on your office or your legal fees for incorporating)

All of this information helps you do a few things. For one, it helps you account for and justify everything you spent business funds on.

Looking at your business expenses also helps you figure out how they correlate with revenue. That makes it easy to find patterns, identify overspending, and see where you can cut down on expenses for next year.

Tax forms and documents

Many of us are far from ready to file our taxes when we go for year end accounting help. Still, it’s a good idea to bring any tax documents and forms you do have ready. Your tax forms are an overview of your financial year—not unlike your business financial reports. They can be helpful in confirming things like self-employment income, spending on contractors, and your small business payroll expenses.

If you have them ready, bring these tax documents to your accountant’s office:

- All 1099-NEC forms and 1099-MISC forms you’ve received from clients or customers

- All 1099-NEC forms you’ve sent to contractors

- All employee W-2 forms and your W-3 form

- All 1099-K forms from third-party financial institutions and payment processors (like Wave)

- Documentation to back up any deductions you plan to claim (like a home office deduction)

- All employment tax returns filed throughout the year - these are typically filed quarterly using Form 941

Questions to ask

Few business owners fall in love with the accounting side of running a business. If your idea of a great year end means handing off paperwork to your accountant and letting them handle the rest, you’re not alone.

You don’t need to have a CPA to have a grasp on your business’ finances, though—and understanding your books can only help your business thrive.

That knowledge starts with getting the skinny from your accountant. Ask the questions below (and any others you have) to better understand the state of your business finances and what you can do to improve them.

How can I optimize my cash flow?

Cash flow is a particularly tough problem for contractors who work on a project-to-project basis and seasonal businesses. No matter how much revenue your business brings in, cash flow is something a lot of businesses, large and small, struggle with.

It’s one thing to turn a profit at the end of the year—it’s quite another thing to maintain a healthy cash flow throughout the year.

Healthy cash flow ensures you can cover your bills and expenses on time and that you won’t go belly up if an unexpected expense pops up. That’s why it’s good practice to look for ways to optimize and improve your cash flow every year, even if you haven’t had a crisis of cash.

Is the legal structure of my business still the best option for me?

Whether your business operates as a sole proprietorship, partnership, limited liability company (LLC), or corporation, there are a lot of benefits and disadvantages to each legal structure.

Even if you worked with a professional accountant to decide on the right structure when you launched, this could change as your business grows and evolves. That’s why it’s an important conversation to have with your accountant every year—to ensure you’re putting your business in the best possible position.

How and where can I grow my profits next year?

For most businesses, you grow by increasing profit. Boosting profit comes down to two things: growing revenue or decreasing expenses—and your accountant can help you explore both avenues.

How should I estimate quarterly tax payments next year?

Entrepreneurs and small business owners who don’t have taxes withheld from each pay check are expected to pay estimated taxes each quarter. As the name implies, these are an estimation based on what your total income is expected to be—meaning they can change a lot from year to year.

It’s important to take a look at your total income for the year, as well as how it matches up with your estimates throughout each quarter. This is the information that will help inform your estimated payments for the following year.

Anything else you want to know

There are a million and one things we could recommend talking with your accountant about. At the end of the day, it all comes down to the information you want and need from them.

Your accountant is more than the person who keeps your books or files your taxes. They’re experienced professionals with a lot of expertise and advice to offer your business. They’ve seen all kinds of businesses and financial situations.

So take advantage of that and don’t be afraid to ask every burning, nagging question you have—your accountant is there to help.

Be prepared for year end accounting

Completing your year end accounting and preparing to close your books is all about wrapping the year up in a nice little bow—then mining your business information for ways you can grow and improve in the new year.

Year end offers key insights that can help you increase revenue, develop a healthier cash flow, save on taxes, and a whole host of other things.

Chapter 3: Filing your self-employment and business taxes

As each year draws to an end, there’s one thing on a lot of minds: taxes.

For small businesses and independent workers, a lot goes into filing your taxes. From parsing all the tax forms you send and receive to figuring out your estimated quarterly taxes for next year, tax season is a busy time and it’s easy for April 15th to sneak up on you.

That’s why it’s always a good idea to get a head start on tax filing as soon as the year ends. Once your annual return is out of the way, you can relax and focus on more exciting things like growing your business.

In this chapter, we’ll talk about:

- Why you should work with an accountant to prepare and file your taxes

- How to find the right tax professional for you

- Documents and records your accountant will need

- How to actually file and pay your taxes

Here we go!

Why you should work with an accountant to prepare your taxes

When it comes to preparing and filing your taxes, today’s small business owners have more options than ever before. You can:

- Scour the internet for tips and best practices and file on your own

- Use tax software like H&R Block to help you prepare your return

- Get a personal H&R Block tax pro to file your taxes for you

- Work with a tax professional, enrolled agent (EA) or certified public accountant (CPA) to handle the prep and filing for you

That being said, we always recommend that you work with a professional to prepare your business tax return. Personal taxes are one thing, but when it comes to your business, hiring a professional accountant, enrolled agent or CPA is a no-brainer.

Tax pros do this stuff for a living—they can ensure your T’s are crossed and your I’s are dotted. Peace of mind and a maximized refund are both worth a lot more than the cost of hiring a professional.

Here are a few other compelling reasons to work with a pro this year.

Self-employment income adds complexity to your return

Self-employed taxpayers can have hundreds of 1099 forms to sift through. Business owners might have dozens of different deductions, each requiring its own set of documentation. Not to mention: math.

Between the complexity of self-employment and business taxes and what’s at stake if you miss something, hiring a tax pro to handle your prep and filing is a no-brainer for entrepreneurs and businesses.

Maximize your refund and get it right the first time

If you’re thinking that a good tax software can handle all of that complexity for you, you’re right…and you’re wrong.

Popular tax software options do make it much easier to get all the right information and documentation in the right places. That being said, tax software can’t maximize your refund the way a human CPA can.

Humans have years or even decades of experience preparing taxes and working with businesses like yours. They can find deductions you didn’t even know you qualify for and identify other ways to lower your tax liability. Humans understand the nuance and loopholes riddled throughout U.S. tax code—better than software can.

Get advice on how to optimize your business and lower your tax liability

Speaking of advice, a professional CPA or accountant can help you figure out ways to lower your total tax liability. Everything from the legal structure of your business to whether you work with independent contractors to how much you pay in quarterly taxes affects your ultimate tax refund or payment.

A lower tax liability means more money that goes back into your business (or maybe funds some much-needed PTO).

Tax pros can also help you set the right expectations for your business taxes. Freelancer Lindsey Peacock talks about a vital mistake she made during her first year as a freelancer—and how it ended up costing her $6,000.

A professional business accountant could’ve saved Lindsey the stress of an unexpected bill by giving her the right information, upfront, about how much she should expect to pay in self-employment taxes.

How to find the right tax accountant for your business

Now that we’ve convinced you to work with a professional tax accountant when you file, let’s talk about how and where to find a good one. Google something like “small business accountant,” you’ll drown in results.

214 million of them, in fact.

How do you filter through that many options and actually find someone you want to work with? To start, you have to know what to look for. Once you know what makes a good tax filing partner, we’ll talk about a few places where you can find a more curated list of options.

What to look for in a small business tax accountant

In the world of business taxes, not all accountants are created equal. Some may be more experienced, more talented, or just a better fit for your particular business—and it’s important that you know how to find the best tax pro for you.

To start, you definitely want to work with a registered accounting professional who’s certified to prepare and file your taxes, like a small business certified tax pro at H&R Block. That might also include a Certified Public Accountant (CPA) or Enrolled Agent (EA). Either way, you can be sure that certified tax preparers know their stuff, and you can trust their experience.

To verify an accountant’s credentials, check out CPA Verify or the American Institute of Certified Public Accounts (AICPA’s) website.

Once you confirm an accountant is certified, there are a few other, more subjective things to consider before working with them.

- Specialty and expertise: Just like your business serves a particular niche, so do tax accountants. Your best bet is to look for a CPA or EA who has plenty of experience working with small businesses—and your type of business (sole proprietorship, freelancer, LLC, etc.), too.

- Experience in your industry: On top of small business expertise, it can help to work with an accountant who has experience in your industry, as well—particularly if your industry has its own unique tax challenges (like ecommerce or real estate).

- Reviews and testimonials: Knowledge and experience are one thing, but how will the tax pro put them to work for you? A good accountant should be able to provide reviews or testimonials from current and past clients. If they don’t have any, that could be a red flag.

- Rates and pricing: When it comes to accounting and tax prep fees, you’ll need to do some research on common rates—both in your local area and for your business situation. Beware of rates that seem too good to be true.

- Easy to work with: Working with your accountant shouldn’t be a painful experience. Look for a pro who’s communicative, friendly, and helpful.

Where to find a good accountant

Now that you know what makes up a good business tax accountant, let’s talk about where to find potential accountants. As we said before, searching Google for a small business accountant is a one-way ticket to overwhelm. The easiest way to sift through your options is to start with an already curated list from the beginning.

An easy, research-free way to get tax help right off the bat is to import your Wave data straight into H&R Block and instantly get connected with a tax pro specialized in small business.

But where else can you find a curated list of qualified accountants and CPAs? Start with your existing network. Ask for referrals from friends, family, and colleagues who own a business or work a side job. That’s the best way to go straight to the most qualified accountants, and your network can give you all the details about what it’s actually like to work with them.

If you don’t find a match through your network, there are several business organizations that should be able to give you a list of certified and local tax professionals. Look for your local Chamber of Commerce or a nearby Small Business Development Center.

Last but not least, try a review website

What to give your accountant

Once you find a small business accountant you can’t wait to work with, it’s time to start gathering up all the documents and other records they’ll need to prepare your taxes.

For small businesses and independent workers, those documents can add up quickly. The average employee just needs to bring the one W-2 form their employer delivered to them. But for the self-employed, sifting through your income, tax paid, and expenses involves quite a few more pieces of paper.

Here’s a list of all the things your business accountant will definitely need:

- Last year’s tax return

- Your business’ Income Statement (also called your Profit & Loss report)

- Receipts for your quarterly estimated payments

- All 1099-NEC and 1099-MISC forms you’ve received from clients or customers

- A copy of any 1099-NEC forms you’ve sent to contractors

- Any 1099-K forms from third-party financial institutions and payment processors (like Wave)

- Documentation to back up any deductions you plan to claim (like a home office deduction, receipts for business expenses)

- W-2 forms for any employees you have and your W-3 form

- Your W-2 form (if you’re also employed or were at some point during the tax year)

- Your employment tax returns for the year

Our list is a good starting point, but it isn’t comprehensive for every situation. To be safe, give your accountant a call before you head to their office so you can be sure you have everything they need.

How to file your taxes

Now that your tax return is ready to rock, how do you actually file your business taxes?

Here’s the short version: if you work with an H&R Block tax professional, EA, or CPA, they can file all your tax forms for you. Typically, filing your taxes is included in the normal fee you pay.

If you decide to go it alone and file your own taxes, you have two choices. The quickest and easiest option is to e-file (for free!) through Free File from the IRS. For the paper lovers among us, you can also still choose to file by mail. You can find the right mailing address on the IRS website or look for the instructions on the last page of your 1040 form.

How to pay your taxes

When you’re ready to pay any balance owed on your taxes, there a lot of options for how to pay.

Online

Again, the quickest and easiest way is to pay online—using your bank account, credit, or debit card. There are a few different ways you can pay your taxes electronically:

- On the IRS website or IRS2Go app

- The Electronic Federal Tax Payment System (EFTPS): You may be familiar with the EFTPS because it’s where you make quarterly estimated tax payments

- Electronic Funds Withdrawal: If you work with a professional tax preparer or tax software, they’ll submit your payment through this method when they file your taxes. If you file yourself using Free File, you can do the same and schedule your payment for anytime up until the due date

By mail

You can also make tax payments through the mail if you’re paying with a check or money order. If you file by mail, too, include the check with your tax forms. Otherwise, mail the check or money order along with:

- Your name and address

- A good daytime phone number

- Your Social Security Number (SSN) or Employer Identification Number (EIN)

- The tax year you’re paying for

You can find the right mailing address on the IRS website or listed in the instructions on your tax forms.

In person

That’s right, you can even pay your taxes in person. There are two ways to submit tax payments in person:

- At your bank, where you can submit a same-day wire transfer or

- With cash at a participating retail store

To pay at your bank, fill out the Same-Day Taxpayer Worksheet and bring it into your bank’s nearest location. Don’t forget: wire transfers usually incur a fee from your bank, so it’s important to find out how much the fee will be before you decide to pay this way.

To pay with cash, you’ll need to visit the Official Payments website to verify your information. Once the IRS confirms your information, you’ll get an email with your payment code, location to pay, and other instructions. Cash payments incur a $3.99 fee.

Staying on the tax department’s good side

Taxes aren’t the most exciting part of running your own business, but they are an important one nonetheless.

By gathering your information together and getting an early start as the year ends, you’ll be in good shape to find the right accountant and maximize your refund—so you can kick back and relax as the tax deadline approaches.

Chapter 4: Handling an audit

As a small business owner, you go to great lengths to make sure you’re complying with all the necessary tax laws and requirements. You save up and organize all your receipts, sort through dozens of 1099 forms, and make payments on time.

So when the government decides to audit your tax return, it can feel a little scary.

Here’s the thing: you don’t need to be afraid of an IRS audit. For starters, audits are relatively rare when you consider the sheer number of tax returns the IRS handles.

The IRS notes that in 2015, audits made up less than 1% of the 150 million returns filed that year.

But if you do wind up in the small percentage of business owners who get audited, you still don’t need to fret.

In the name of less audit stress, this chapter will cover:

- What it means to be audited by the government,

- How to prepare for an audit before it happens,

- What to do when you receive an audit notice, and

- What you’ll need to give the auditor.

Then we’ll finish off with a story about why you really truly don’t need to sweat an audit. Let’s get to it!

What does it mean to get audited by the IRS?

Why your business might get audited

There are a lot of reasons the IRS might audit your business tax return—and very few of them mean the government thinks you committed criminal tax fraud. Remember: an audit isn’t an accusation. It just means the IRS wants to take a second look at your taxes to ensure everything is accurate, and fix anything that isn’t.

The key to getting through an IRS audit unscathed is to be prepared for it (more on that later!) It can help to understand why the government might audit your business, so you can anticipate an audit and take steps to avoid it.

Here are a few common things that can trigger an IRS audit:

- You made income that wasn’t reported on your return

- Your business suffered larger-than-ordinary operating losses

- There were errors, inconsistencies, or omissions in your return

- You deducted lavish business expenses for meals and entertainment

- Your reported income dropped sharply from one year to the next

- You have a large amount of cash receipts

- You keep money in a foreign bank account

That being said, the IRS also conducts random audits that can happen even if none of the red-flags above apply to you or your business. That’s why it’s important to always be prepared with documentation to back up your income, expenses, and deductions.

How to be prepared for an audit

Being prepared to face a government audit is all about organization and proof. Here are the most important tips you should follow to ensure you’re ready for an audit if and when it arrives:

- Keep your business and personal finances separate: This is a good tip to follow even if all it ever does is simplify your bookkeeping. Keeping your finances separate makes it easier to organize and keep track of your business income and expenses, so you can prove your income, expenses, and deductions in the case of an audit.

- Track every penny: In the same vein, it’s important to keep track of every penny that flows into and out of your business. Not only does this enable you to claim all the deductions you qualify for, but it makes for concrete documentation of your business income and expenses, which comes in handy when an audit questions their veracity.

- Stay organized throughout the year: One of the most common mistakes small business owners make is failing to save and organize their business receipts, invoices, and reports throughout the year.

- Work with a tax professional to prepare and file: Back in Chapter 3, we talked about the importance of working with a professional accountant, H&R Block tax pro, EA, or CPA to file your taxes. An added benefit of working with a professional is having a partner to help you through the audit process and work with the IRS on your behalf.

What to do if you receive an IRS audit notice

No matter how prepared you are for a tax audit, it’s normal to feel a little panicky when an audit notice arrives in the mail. For starters, just take a breath and remind yourself that you’ve prepared for this.

After that, these simple steps are the best way to get started responding to and working through an audit.

Step 1: Make sure the audit is legitimate

Verifying the authenticity of your audit notice might seem like a wasted first step, but it’s actually really important. The IRS is a favorite of scammers because they know people are likely to react quickly and without too much thought because we’re all secretly terrified of the IRS.

Don’t be that person—there are a few obvious calling cards of an audit scam.

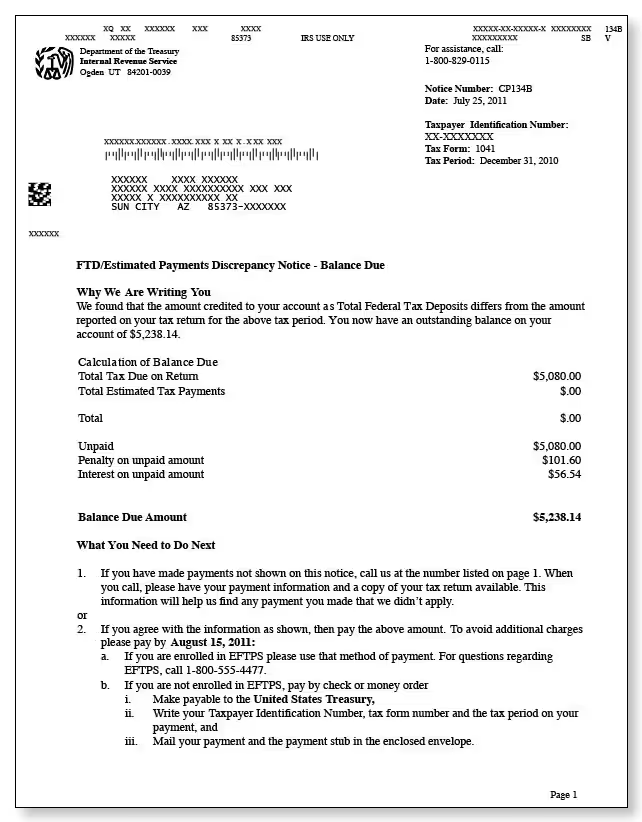

The biggest red flag has to do with the medium of the notice. The IRS, for security reasons, will only ever initiate contact via a mailed letter to your home or business address. If you get a phone call, voicemail, or email about an audit, it’s a fake.

A genuine letter from the IRS may look something like this:

If you’re ever unsure whether an audit notice is legitimate, your best bet is to contact the IRS directly. You can call the agency at 800-829-1040 or visit their website for help confirming the letter is for real.

Step 2: Contact your tax pro, CPA, EA or accountant

Once you know the audit notice is legitimate, your very next step should be to contact your accountant, EA or CPA. Whether they prepared and filed your tax return or you did it yourself, it’s absolutely vital to have a professional on your side during the audit process.

For one, your tax pro may have been through an audit before. They’ll know how to handle one and what to expect. They can also help you decipher why you’re being audited—if it’s an actual mistake or just a routine audit to verify the information in your return.

When it comes to working with the IRS, it’s always best to have a professional in your corner—because the IRS auditor is a professional, and their job is to get all the tax money the government has a claim to.

Many small business owners choose to sign over power-of-attorney to their accountant, EA or CPA, too. That enables them to interact with the IRS directly and on your behalf, so you can take a step back and focus on running your business.

Step 3: Gather all documentation requested by the IRS

When the IRS conducts an audit, they’re essentially looking for proof. That's why it's so important to keep track of receipts; they're backup to your business expenses, documentation to show your eligibility for the deductions you claimed, and verification of your income.

As we discussed above, the number one key to surviving an audit is to have that documentation organized and ready to go.

What you’ll need to give to the auditor

Now, let’s talk about what you might need to give to the auditor. Typically, your audit notice will request specific information or documents from you. If that’s the case, bring those documents plus anything else relating to the tax year in question. That includes:

- Receipts and invoices for income and expenses

- Bank statements and canceled checks

- Accounting books and ledgers

- Hard copies of tax-prep data

- Leases or titles for business property

Step 4: Let your CPA take it from there

Once you’ve spoken with your accountant and handed over all the necessary documents, it’s time to take a step back and let your CPA handle the rest.

As we said above, the IRS auditor is a professional whose job is to secure all the tax money the government’s owed. You aren’t a tax professional, and the auditor is. It’s easy to get tripped up or confuse things.

That’s why, to be safe, it’s best to limit your contact with the auditor and let your CPA take care of communicating and working with them.

Story time: Why you don’t need to fear the audit

Between the horror stories of audits taking over people’s lives to the very real fear of math, it’s easy to panic when that audit notice lands in your mailbox.

But as one of our Wave customers learned, going through a government audit isn’t as scary as it’s made out to be.

After receiving an audit letter in the fall, their gut reaction was much the same as most small business owners: “My first thought was, ‘What did I do wrong?’ Or, maybe more accurately, ‘What didn’t I do right?’ Could there have been a moment where I did something not quite by-the-book, unintentionally?”

As most do these days, they took to Google to find comfort in the stories of other people who’d been through the same situation. They learned three important things about going through a government audit:

- You don’t have to be afraid

- Being organized matters… a lot

- Mistakes can be fixed

“The audit experience could have been much more difficult,” they shared, “if I hadn’t kept such good records.”

Dealing with the government can sometimes feel like a zero-sum game—but the vast majority of IRS audits happen because of small errors that are easily solved through correspondence alone.

“The biggest lesson I learned from this whole experience was that mistakes happen, even when you have the best of intentions… but I was surprised to find that most were fixable,” they said.

As long as your tax documents are organized and up-to-date, you’re in good shape to resolve the audit pretty painlessly.

Handling an audit like a pro

As attorney Frank Gohlke tells Business News Daily: “Keep proper documentation, and only deduct ordinary and necessary business expenses that are allowed by the IRS. Even if you are selected for an audit, you will know you have nothing to worry about.”

IRS audits aren’t fun, but they don’t have to take over your life or cause unnecessary stress. If you stay organized and let your accountant or CPA handle the auditor, you’ll be in good shape to survive the audit and maybe even learn a little something along the way.

Chapter 5: Staying organized all year long

The National Small Business Association notes that around 20% of small business owners spend up to 120 hours on taxes each year—that’s a lot of time spent away from actually running your business.

That’s why business owners who don’t dread tax season have one thing in common: they keep their books and finances in order all year long. That way, when the year ends, they’re in the best possible shape to take stock of their business and start preparing for tax season.

Because year end accounting is about more than just closing your books on the year. It’s an opportunity to look at your business’ performance and financial health—so you can set goals and improvements for the upcoming year. Staying organized and planning ahead also helps you get a jump on activities and record-keeping, lowering your business’ tax liability next year.

In this chapter, we’ll talk about:

- Why neglecting your books is a bad idea

- Documents, records, and reports to keep track of

- Tips for staying organized and on top of your books all year long

Let’s get to it!

Why you shouldn’t neglect your books

We briefly touched on some of the key benefits to staying organized and on top of your business accounting. In addition to losing out on those vital benefits, there are also some important reasons why neglecting your books can cause you harm. Here are a few of the biggest reasons.

Disorganized books add time and stress at the end of the year

There’s no getting around organizing your receipts come tax season—we all have to sit down and file our taxes no matter what. If you’ve neglected your books all year, you’re only adding undue stress and time to this process at year’s end.

Cash flow crises can sneak up on you

Your business’s survival depends on your ability to make investments and pay bills when you need to. If you aren’t properly tracking the money that flows into and out of your business, it’s easy for a crisis of cash flow to hit when you’re least equipped to handle it. Instead, steady bookkeeping helps you keep a pulse on the financial health of your business.

You might miss important deadlines throughout the year

As small business owners know, tax time comes more than once a year. If you aren’t keeping track of your books, deadlines like your quarterly tax payments can easily sneak up on you or even sneak by without you noticing.

You might miss out on tax deductions your qualify for

No matter what tax deductions you’re eligible for, you can only claim those you have documentation to back up (in case of an audit)—if you aren’t staying on top of those expenses and deductions, you could lose out when it comes time to file.

What to store and keep track of

Now that you’re convinced that it’s important to keep your books and records up-to-date throughout the year, let’s talk about what, exactly, you need to keep track of. Current books contribute to financial analysis of your business and tax filing, so there are a lot of different things you should keep track of, including:

- Gross receipts from product/service sales

- Returns and allowances

- Business account interest

- Cost of inventory

- Cost of materials and supplies

- Advertising expenses

- Utility costs (like landline phones, fax lines, etc.)

- Travel expenses (including mileage costs)

- Commissions paid to subcontractors

- Depreciation on business assets

- Cost of business insurance

- Office supply costs

- Wages and salaries

- Receipts for charitable donations

- Medical expenses

- Any pay stubs

- Investment summaries

- Property tax bills

Tips for staying on top of your books throughout the year

It can seem daunting to keep track of all these documents for the entire year. That’s why we pulled together some key tips for staying on top of your books without sinking unnecessary time and stress into the process.

Set up efficient systems

Once you know what you need for your year-end filing next year and beyond, it’s time to put systems in place to track your data. That means stashing away random receipts in a shoebox is no longer an option.

Freelancers and small business owners can use accounting software to keep track of revenues and expenses. To stay ahead of next year’s tax filing, establish some good habits like:

- Uploading digital receipts directly to small business software like Wave* to categorize and monitor expenses

- Taking a picture of receipts with your phone to digitize them for safe-keeping

- Keeping track of bills to see how much your business is spending in each category (like website hosting fees versus rent for your office space)

- Generating and managing invoices in one place

- Setting up automated invoicing for recurring invoices

- Scanning and saving important tax documents like investment summaries and property tax bills to a folder on your computer

Schedule regular check-ins

The lead up to your year-end filing shouldn’t be the only time you check in on your business finances.

To avoid surprises and to run your business efficiently, maintaining visibility into your finances is crucial. And once you’ve gathered the appropriate paperwork and established some expense tracking systems, “checking under the hood” of your business becomes far simpler.

Set some time aside in your calendar once a month to dive deep into revenues and expenses. This simple practice can prevent any last-minute surprises from popping up at tax time. Create some calendar alerts to ensure you don’t forget.

Regularly reviewing your books can also empower you with insights to run your business better. For example, a quick look at your business finances could reveal that the average time it takes for clients to remit payment is 60+ days. To curb outstanding invoices and improve cash flow, you can set up automatic reminders for clients to pay their invoices after 15 or 30 days.

And making this kind of high-impact change isn’t that difficult—it can come from a little bit of data and a quick review of your books.

Plan ahead for major changes

In the midst of all this preparation, you’re likely thinking about the things to come in the year ahead. What major changes will you and your business celebrate in the next 12 months?

Some of the milestones that could affect your filing include:

- Getting married

- Having children

- Retiring

- Major equipment purchases

- Buying/selling commercial or personal property

All of these events can affect your taxable income and may require additional documents when submitting your taxes.

To help offset any increase in taxable income from these major milestones, plan ahead with the following tactics:

- Maximize retirement contributions: Saving for retirement not only prepares you for living well in your golden years, but it also lowers your taxable income. Contributing to a qualified savings plan like a 401(k) or an IRA can help you take advantage of the powers of compound interest while also saving your business some serious cash on your tax bill.

- Make charitable donations: Helping out qualified non-profits is a win-win for businesses and charities alike. If you make a donation before the end of the year, you can deduct the contribution from your year-end filing to reduce your tax burden.

Staying organized for a better year end

During the year, it’s easy to rationalize letting your books slip. You’re busy, your customers and employees need you, you’re focused on growing the business. But at the end of the day, maintaining up-to-date and accurate books and records is one of the most powerful tools you have to grow your business.

From making tax time easier to helping you better understand your business finances and grow, staying organized all year long just makes sense for smart business owners.

Plus, with all your bookkeeping nice and organized, it makes it so much easier to import your Wave data right into H&R Block and quickly and painlessly get set up with a tax pro, who can either file for you or just help you when you need it. Simply log into Wave and click the “Tax Filing” link in the navigation menu to get started.

*Wave’s receipts feature is a paid product that requires a subscription. Pricing information can be found here.

**We use Plaid to facilitate bank connections. Not all financial institutions are supported so we can’t guarantee that you will be able to connect an account. Check Plaid's troubleshooting guide for more information or learn more about how bank connections work at Wave.

(and create unique links with checkouts)

*While subscribed to Wave’s Pro Plan, get 2.9% + $0 (Visa, Mastercard, Discover) and 3.4% + $0 (Amex) per transaction for the first 10 transactions of each month of your subscription, then 2.9% + $0.60 (Visa, Mastercard, Discover) and 3.4% + $0.60 (Amex) per transaction. Discover processing is only available to US customers. See full terms and conditions for the US and Canada. See Wave’s Terms of Service for more information.

The information and tips shared on this blog are meant to be used as learning and personal development tools as you launch, run and grow your business. While a good place to start, these articles should not take the place of personalized advice from professionals. As our lawyers would say: “All content on Wave’s blog is intended for informational purposes only. It should not be considered legal or financial advice.” Additionally, Wave is the legal copyright holder of all materials on the blog, and others cannot re-use or publish it without our written consent.

Read next