How bank reconciliation keeps your business on track

Every small business owner knows that even tiny mistakes can snowball into major headaches. That missed $200 invoice you forgot to follow up on? It could mean frantically hunting for loose change when your laptop decides to take a coffee bath. The expense you accidentally entered twice because Monday brain is real? Come tax season, you'll be staring at your numbers like they're written in ancient hieroglyphics.

These seemingly small bookkeeping mistakes can cost small businesses big money and sanity each year. The good news? There's a simple habit that can help you catch these pesky issues before they multiply: reconciliation.

By the end of this post, you'll understand exactly what reconciliation is, why it's your business's financial superhero, and how to do it without breaking a sweat using Wave's updated reconciliation feature. Plus, you'll discover how this straightforward process can save you stress, money, and those 3 AM “Did I accidentally commit tax fraud?” panic attacks.

What is bank reconciliation?

Bank reconciliation is the process of comparing your bookkeeping records with your bank statements to make sure everything matches up. Think of it as double-checking your work; you're verifying that the money coming in and going out of your business accounts is accurately reflected in both places.

Here's how it works in practice: You take your bank statement and line it up with your bookkeeping records for the same time period. Every deposit, withdrawal, check, and fee should appear in both places. When they don't match perfectly, you investigate why and fix any discrepancies.

Make it a habit to reconcile your accounts every time you receive a bank statement, which is typically monthly for each bank account or credit card account you have. This regular check-up ensures your financial records stay accurate and up-to-date.

Why is bank reconciliation important for small businesses?

Bank reconciliation is like having a bouncer for your books; it makes sure nothing sketchy gets past, nothing important goes missing, and everything stays legit.

Reconciling your accounts regularly can help you:

- Keep accurate financial records

- Catch errors early

- Detect missing invoice payments

- Stay ready for tax season and audits

- Identify potential fraud

Let's dive deeper into each of these benefits.

Keep accurate financial records

Reconciliation helps ensure that your cash flow statement, profit and loss statement, and balance sheets actually reflect reality. Without this verification process, you might be making business decisions based on incomplete or incorrect information… not exactly a recipe for success.

This process helps you avoid the "Did I already count that?" dilemma and gives you a good view into where your money's actually going.

It also helps you spot discrepancies early, before they spiral into bigger problems. When you notice issues right away, you have the opportunity to investigate and tweak your business operations.

Detect errors early

We're all human (unless you happen to be a highly-intelligent golden retriever), and data entry mistakes happen. Reconciliation helps you catch and correct these slip-ups before they cause major problems.

Error-free records are absolutely critical when tax season rolls around. If your records are wonky, you could end up under-reporting or over-reporting your earnings. This opens the door to fees, penalties, audits, and other headaches that no small business owner wants to deal with.

By catching mistakes early through regular reconciliation, you can fix them quickly and get back to what you do best.

Detect missing invoice payments

Here's a scenario that might sound familiar: You mark an invoice as paid because your client pinky-promised they sent it… but their bank had other plans, and it was never processed. Without reconciliation, you might not notice this missing payment for weeks or even months.

When you reconcile your accounts, you'll immediately spot that the payment deposit is nowhere to be found in your bank statements. Staying diligent allows you to reach out to your client right away and resolve the payment issue before it affects your cash flow.

Stay ready for tax season and audits

Nobody enjoys tax season scrambles. Nobody enjoys the thought of a tax audit either! Reconciliation helps you keep your documentation clean and organized throughout the year, so you're not stuck doing months of catch-up work when tax season or an audit rolls around.

By performing account reconciliations regularly, you avoid adding hours of extra work when tax time arrives. Your records are already accurate and ready to go, which means less stress for you!

Identify fraud

Unfortunately, financial troublemakers can target any business. Regular reconciliation helps you catch suspicious activity early.

When you review your bank statements against your records, unfamiliar transactions will stand out right away. Maybe it's a subscription you forgot about, or maybe it's something more serious that requires quick action.

If you see a transaction that looks fishy, always investigate! Catching it early saves you money and prevents further hiccups.

What are common errors you might find when reconciling your accounts?

Even with the best intentions, discrepancies between your books and bank statements can pop up. Here are the most common errors you're likely to encounter:

Missing transactions: Your bookkeeping records are missing transactions that appear on your bank statements. This often occurs when sneaky automatic payments or bank fees slip by unnoticed.

Extra transactions: Your bookkeeping records contain transactions that don't appear on your bank statements. This might happen if you logged something that got canceled or accidentally created a duplicate entry.

Duplicate transactions: Your bookkeeping records contain multiple versions of a single transaction that appears once on your bank statement. This is one of the most common mistakes, especially if you're manually entering transactions.

Incorrect statement balance: Your bookkeeping records show a different ending balance than what appears on your bank statement. This could be due to timing differences or cumulative errors from previous periods.

Incorrect transaction dates: Your bookkeeping records contain transaction dates that don't match the dates on your bank statement. This can happen if your bookkeeping records use the transaction date, while your bank uses the posting date. Time differences for online payments, outstanding checks or deposits, bank errors, or human error can also cause this issue.

Don't worry — these errors are normal and fixable. In the next section, you'll learn exactly how to address each of these issues using Wave's reconciliation feature.

How to reconcile your accounts in Wave: A step-by-step guide

Wave's updated reconciliation feature makes the entire process straightforward and intuitive. Here are the four key steps to reconcile your accounts in Wave:

- Gather your bank statements

- Create a reconciliation period

- Match your transactions

- Fix unreconciled transaction periods

To reconcile an account, you'll open or create a reconciliation period, then match the transactions in Wave to the transactions on your bank statement. Your bank statement should list all transactions for the date range and the closing balance.

Step 1: Gather your bank statements

Before you start, make sure you have either physical or digital copies of your bank statements handy. Organization is key here — create a simple checklist of all the different statements you need ready each time you reconcile.

Include the following in your checklist:

- Your different bank and credit card accounts

- Statement dates for each account

- Statement frequency for each account

For example, your credit card statement might be ready on the 18th of each month, while your checking account statement might be ready on the 1st. Keeping track of these different schedules helps you stay on top of your reconciliation routine.

Step 2: Create a reconciliation period

Wave makes it easy to organize your books and start reconciling right away. Once you're logged into your Wave account:

- On the left-side menu, click Accounting > Transactions

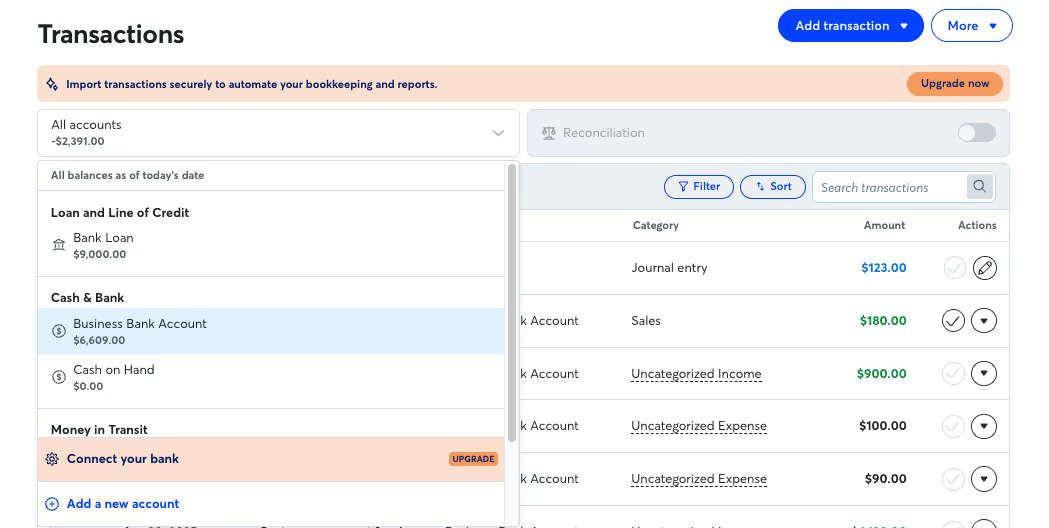

- Click All accounts to open the dropdown menu, and select the account you want to reconcile

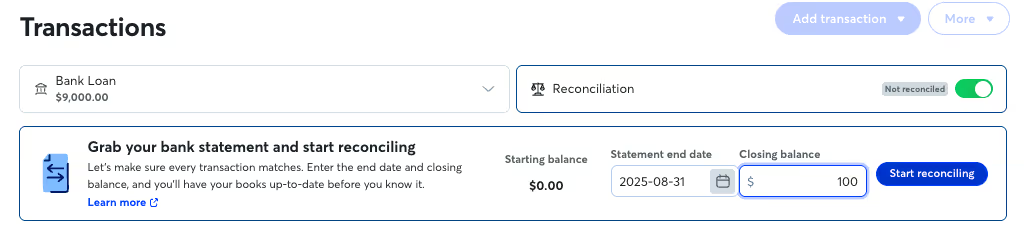

- Next to Reconciliation, switch the reconciliation toggle to On

- To create a new period, enter the end date and closing balance from your bank statement, then click Start reconciling

This sets up your reconciliation period with all the information Wave needs to help you match your transactions.

Step 3: Match your transactions

This is where the magic happens. Wave will show you all your transactions and help you match them with your bank statement.

If your closing balance on the bank statement is the same as your Wave balance, Wave will do the heavy lifting for you. A pop-up will appear with two options: click Reconcile automatically to have Wave match all transactions in the period, or click Reconcile manually if you prefer to review each transaction yourself (control freak? We don't judge).

At the top of your reconciliation period, you'll see the important stuff: the number of unmatched transactions, the closing balance from your bank statement, the matched balance in Wave, and the difference between the two balances.

To mark a transaction as matched, click the balance icon under the Match column. To unmatch a transaction, simply click the balance icon again. As you match transactions, both the Matched balance and the Difference amount will update in real-time.

Your goal is to get the Difference amount to zero. Once the matched balance and statement balance are identical, and there are no discrepancies between transactions and your bank statement, you can click End Reconciliation to complete the period.

If you have pending transactions that don't appear on your current bank statement, don't worry. You can leave them unmatched for now; they'll show up in the next reconciliation period for matching.

And that’s it — you’re done!

OPTIONAL: Fix unreconciled transaction periods

Sometimes you'll find periods that need a little extra TLC. Wave makes these easy to spot: When there's an issue, you'll see a red banner above the reconciled period indicating that it needs your attention.

🔥Hot tip: The system shows only one problematic period at a time because it wants you to fix them in chronological order.

To fix the unreconciled period:

- In the red banner, click Fix it. This takes you directly to the period that needs attention.

- Compare your transactions in Wave with your bank statement for the same time period.

Here's how to resolve the most common discrepancies:

Missing transactions: Click Add Transaction at the top of the page to enter the missing transaction.

Incorrect transactions: Click on the transaction to edit any incorrect information, such as the amount, date, or description.

Duplicate transactions: Select the checkboxes to the left of the duplicate transactions, then click the merge icon at the top of the transactions list.

Incorrect statement balance: Click the pencil icon beside the Closing balance amount, enter the correct closing balance, and click Save.

Pending transactions: If a transaction appears in your reconciliation period but not on your bank statement, Wave might be using the transaction date instead of the posting date. Click End reconciliation, then Reconcile period anyway. You'll match this transaction in the next reconciliation period.

Extra transactions: Made a mistake? Select it and click the checkbox to the left of the transaction, then click the trash can icon to delete it. But be careful—deleted transactions are gone forever, like that leftover pizza you should have taken to go.

Check out our Help Center article for more information.

How often should you reconcile your accounts?

The golden rule: reconcile at least monthly. This matches most bank statement cycles and keeps you on top of things without it becoming a full-time job.

If you have multiple accounts or a high volume of transactions, you might want to reconcile more often — weekly or even daily for your most active accounts. Find a rhythm that works for your business size and doesn't stress you out.

Make sure to reconcile monthly for each account that generates a monthly statement. This includes checking accounts, savings accounts, credit card accounts, and any other financial accounts your business uses.

How Wave makes reconciliation easy for your business

Wave's Pro Plan takes the heavy lifting out of bookkeeping by safely and securely importing your business bank transactions automatically. This means less manual data entry and more time to spend on what you love about running your business.

With automatic transaction import, reconciliation becomes less "data entry marathon" and more "quick double-check." All you need to do is reconcile to make sure everything matches up! It's like having a bookkeeping assistant who's always on the job.

If you hit any snags, Wave Advisors are real accounting pros who can jump on a video call and walk you through solutions using your actual Wave account.

Get started with bank reconciliation today

Bank reconciliation might sound about as exciting as watching paint dry, but it's actually one of the smartest habits you can pick up as a small business owner. Regular reconciliation keeps your financial records squeaky clean, catches problems before they become expensive disasters, and gives you the peace of mind that comes with actually knowing where your business stands.

Remember the perks: accurate records, early problem detection, fraud prevention, and a less stressful tax season. These benefits build up over time, making your business tougher and your life as a business owner way less stressful.

Wave's updated reconciliation features make the entire process straightforward and manageable. Whether you're reconciling for the first time or looking to streamline your existing process, Wave has the tools you need to keep your books accurate and organized.

Ready to get started? Sign up for Wave and experience how simple bookkeeping can be. If you want premium features like automatic transaction import, consider Wave's Pro Plan to save even more time on your financial management.

And if you want hands-on expertise to guide you through the process, book a call with a Wave Advisor. These accounting professionals are here to help you build the strong financial foundation your business deserves.

Your future self (especially during tax season) will thank you for making reconciliation a regular part of your business routine!

(and create unique links with checkouts)

*While subscribed to Wave’s Pro Plan, get 2.9% + $0 (Visa, Mastercard, Discover) and 3.4% + $0 (Amex) per transaction for the first 10 transactions of each month of your subscription, then 2.9% + $0.60 (Visa, Mastercard, Discover) and 3.4% + $0.60 (Amex) per transaction. Discover processing is only available to US customers. See full terms and conditions for the US and Canada. See Wave’s Terms of Service for more information.

The information and tips shared on this blog are meant to be used as learning and personal development tools as you launch, run and grow your business. While a good place to start, these articles should not take the place of personalized advice from professionals. As our lawyers would say: “All content on Wave’s blog is intended for informational purposes only. It should not be considered legal or financial advice.” Additionally, Wave is the legal copyright holder of all materials on the blog, and others cannot re-use or publish it without our written consent.

Read next